The GI Bill is one of the most generous and comprehensive education benefits programs in the United States. Offered by the Department of Veterans Affairs (VA) it provides financial assistance to veterans service members, and their families pursuing higher education or job training. But what exactly does the GI Bill pay for?

In this detailed guide, we’ll walk through the various provisions covered under the GI Bill and how you can maximize your benefits.

A Brief History of the GI Bill

The GI Bill has an illustrious history dating back to World War II. Officially known as the Servicemen’s Readjustment Act of 1944, it was passed to help veterans transition back to civilian life after the war.

Over 16 million veterans of World War II used the original GI Bill to go to college, start businesses, and buy homes. In the years after World War II, the bill helped build the American middle class.

The GI Bill has been renewed and expanded several times since. Today, there are a few different GI Bill programs available based on your military background:

- Post-9/11 GI Bill – For veterans who served on active duty after Sept 10, 2001

- Montgomery GI Bill – For veterans who enlisted and served for 2+ years before 9/11

- Reserve Educational Assistance Program (REAP) – For reservists who served after 9/11

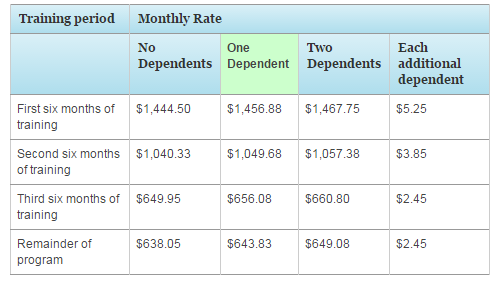

- Survivors’ and Dependents’ Assistance (DEA) – For spouses and children of disabled or deceased veterans

In this article, we’ll focus on the provisions covered under the Post-9/11 GI Bill, which is the most widely used education program today.

Post-9/11 GI Bill Benefits Overview

The Post-9/11 GI Bill provides financial support for education and housing to individuals who have served on active duty for 90 days or more after September 10, 2001.

Depending on your length of service, you can receive up to 100% of the benefits, which includes:

- Full tuition & fees payment

- Monthly housing allowance

- Annual books & supplies stipend

- One-time rural benefit payment

- Yellow Ribbon Program payments

- Transferability to dependents

Next, let’s look at each of these benefit provisions in detail.

Tuition & Fees Coverage

The Post-9/11 GI Bill pays up to the full cost of in-state tuition and fees at public colleges and universities.

For 2022-2023, the maximum coverage is:

- $26,804 per academic year for veterans and dependents

- $28,516 per academic year for active duty servicemembers

If you attend a private or foreign school, the GI Bill covers up to $26,804 annually.

If your tuition and fees exceed the GI Bill limit, your school may offer a tuition relief program (i.e. Yellow Ribbon) to help cover the gap, which we’ll discuss more later.

The tuition benefit is paid directly to your college on your behalf after you’ve enrolled.

Monthly Housing Allowance

For an E-5 with dependents, the Post-9/11 GI Bill gives them a monthly housing stipend based on the military’s Basic Allowance for Housing (BAH) rates.

Your housing allowance will depend on where your school is located, not where you currently live.

Here are the 2022 monthly housing rates for a few sample locations:

- Phoenix, AZ – $2,209

- Orlando, FL – $1,839

- Chicago, IL – $2,169

- New York, NY – $3,657

This allowance helps cover your living expenses while enrolled in school. It is paid directly to the student at the beginning of each month.

To receive the full housing amount, you must be enrolled more than half-time. Active duty service members and spouses using transferred benefits are not eligible.

Annual Books & Supplies Stipend

Every academic year, you can receive up to $1,000 as a books and supplies stipend. This helps cover costs for textbooks, laptops, and other equipment needed for your classes and coursework.

This payment is prorated based on your enrolled credits. You’ll receive up to $41.67 per credit hour, with a maximum of $1,000 per year.

The books stipend is paid directly to the student at the beginning of each term. You can use this money any way you like.

One-Time Rural Benefit Payment

If you reside in a rural area, you may be eligible for a one-time $500 benefit payment to assist with educational expenses.

To qualify, your home address must be outside a “military base, non-metropolitan county, or community of 50,000 people or less.” You can check your eligibility when applying for GI Bill benefits.

This rural stipend is paid on top of your normal tuition, housing, and book benefits.

Yellow Ribbon Program

The Yellow Ribbon Program helps veterans pay for costs exceeding the GI Bill coverage at their college.

Here’s how it works:

Your school voluntarily enters an agreement with the VA to cover a portion of the excess charges above the annual GI Bill limit. The VA then matches the school’s portion dollar-for-dollar.

For example:

Tuition & Fees: $40,000

GI Bill Coverage: $26,804

Remaining Cost: $13,196

Under a Yellow Ribbon agreement, your school covers $6,598 of the overage. The VA then matches that amount, fully covering the $13,196 gap.

Thousands of schools participate in the Yellow Ribbon Program, including many top universities like Duke, NYU, and USC.

You can use the GI Bill Comparison Tool to find Yellow Ribbon schools near you.

College Fund

In addition to the education benefits above, military members who serve for at least 2 years can earn up to $100 per month that the VA will match 8:1 in a special College Fund account.

For example, if you put in $100 per month for 12 months ($1,200 total), the VA will add $9,600 to your account for college for a total of $10,800.

This College Fund money can be used together with your normal GI Bill tuition benefit. It provides a nice boost that can help cover additional education costs.

To receive the College Fund, you need to open a special VEAP or GI Bill contribution account while serving. The matching VA funds do not expire.

Rural Benefit Payments

If your home of record is a rural county with under 7,000 residents, you may qualify for an extra one-time payment of $500 within 6 months of leaving the military.

To receive this rural benefit, apply for it when you apply for your overall GI Bill eligibility.

Transferability to Dependents

One of the most valuable features of the Post-9/11 GI Bill is the ability to transfer unused benefits to your spouse or children.

To transfer your GI Bill:

- You must have completed at least 6 years of service in the armed forces and agree to serve an additional 4 years.

- You can transfer benefits to your spouse, children, or a combination.

- Children must be enrolled in DEERS and are eligible until age 26.

- The amount transferred is limited to the amount of unused benefits you have available.

Over half of GI Bill recipients today use transferred benefits from a family member. This provision allows veterans to share the educational opportunity with loved ones.

Understanding all that your GI Bill offers is the first step to maximizing its value and achieving your academic goals.

Ways to Maximize Your GI Bill Benefits

Now that you know what’s covered, here are some tips to make the most of your benefits:

Complete certifications/training while active duty – Take advantage of free tuition for military education and training to save your GI Bill for college.

Attend public in-state schools – You’ll get full tuition at public colleges in your home state. Private and out-of-state schools often cost much more.

Finish your degree quickly – The GI Bill provides benefits for up to 36 months. Finishing faster means you use less of your eligibility.

Consider Yellow Ribbon schools – Yellow Ribbon funding can help cover costs if your tuition exceeds GI Bill limits.

Use tuition assistance “top up” – If offered by your branch, contribute the $600 maximum to receive the highest value.

Take maximum course loads – Full-time students receive larger housing allowances. Take at least 12 credits per term.

Use every benefit available – Don’t leave any benefits on the table. Understand what’s available through your GI Bill.

Complete internships/apprenticeships – Some programs offer additional housing allowance payments when including work training.

**Transfer

How do I get these benefits?

You’ll need to apply.

The benefit amount depends on which school you go to, how much active-duty service you’ve had since September 10, 2001, and how many credits or training hours you’re taking.

Note: If you use Post-9/11 GI Bill benefits, you’ll need to verify your enrollment every month to keep getting a monthly housing allowance or kicker payments.

How many total months of VA education benefits can I get?

You may be able to get a maximum of 48 months of VA education benefits—not including Veteran Readiness and Employment (VR&E) benefits. But many applicants are eligible for only 36 months.

GI Bill Housing Allowance Explained (BAH)

FAQ

Does the GI Bill cover 4 years of college?

How much will I get from the GI Bill monthly?

Is using the GI Bill worth it?

What are GI Bill benefits?

GI Bill benefits help you pay for college, graduate school, and training programs. Since 1944, the GI Bill has helped qualifying Veterans and their family members get money to cover all or some of the costs for school or training. Learn more about GI Bill benefits on this page—and how to apply for them.

How much does the GI Bill pay for college?

It provides up to full college tuition for public and in-state schools, and more than $25,000 per year at private or foreign schools, as well as money for housing and books. Unlike the Post-9/11 GI Bill, benefit payments will be made directly to you, and you must serve active duty for at least two years.

How does the GI Bill work?

Then when a student is attending college, it pays a set dollar amount per month directly to the student. The Post-9/11 GI Bill doesn’t require an upfront contribution and covers tuition at public colleges and universities, paying the school directly, and up to a certain amount at private institutions. It also provides a housing allowance.

Does the GI Bill cover tuition & stipends?

Yes, the amount of tuition and stipends paid under the Post-9/11 GI Bill will vary depending on your school, number of classes taken, and your length of post-Sept. 10, 2001, active-duty service. Here is a quick reference showing the percentage of total combined benefit eligibility based on the following periods of post-9/11 service: