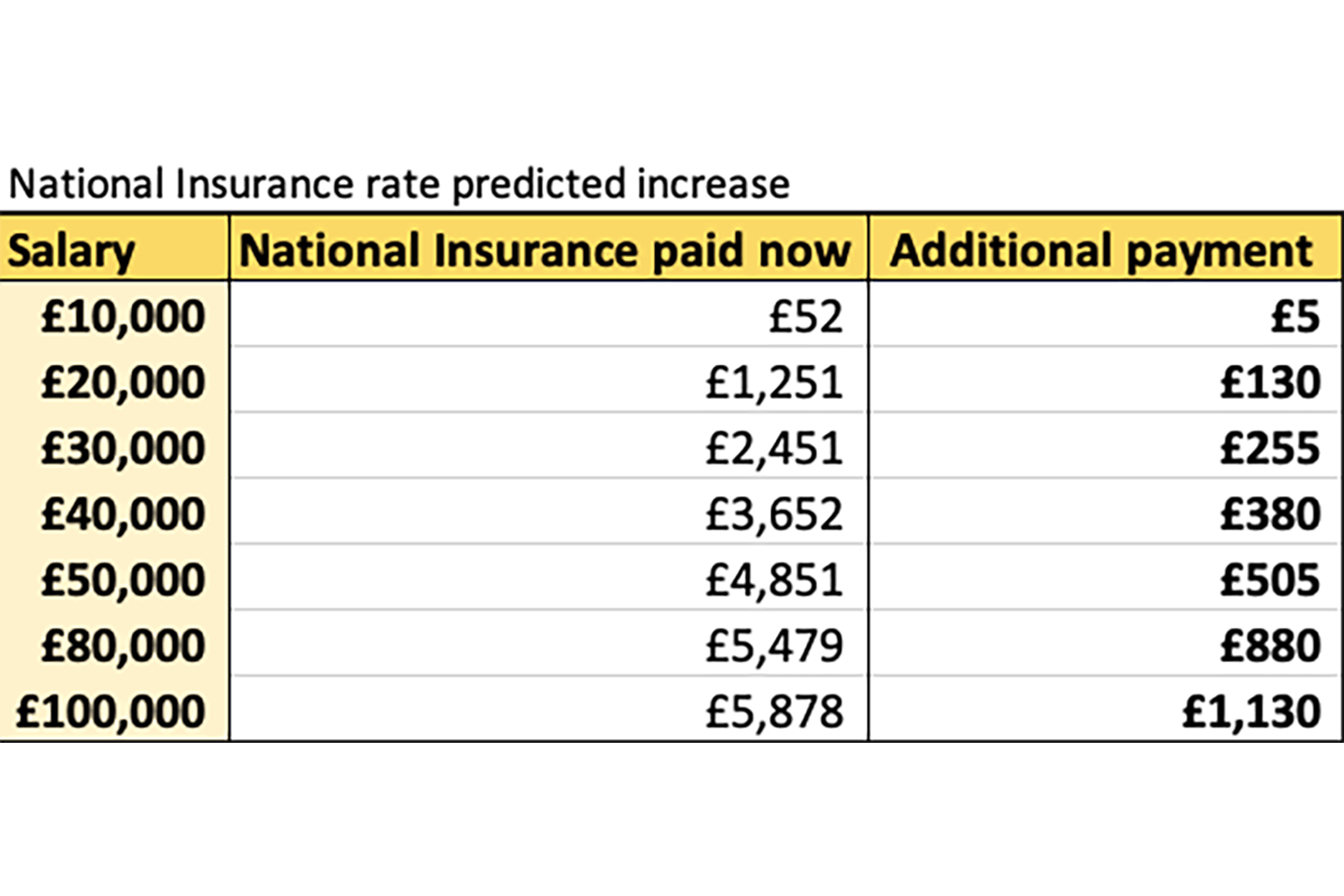

As you approach retirement age, the question of whether you still need to pay National Insurance contributions often arises. This article aims to provide a comprehensive understanding of the rules surrounding National Insurance payments once you reach the State Pension age in the United Kingdom.

Understanding the State Pension Age

Before delving into the specifics of National Insurance contributions, it’s essential to understand the concept of the State Pension age. The State Pension age is the age at which individuals become eligible to receive their State Pension from the government. This age varies based on your date of birth and is regularly reviewed by the government.

Currently, the State Pension age for men and women is gradually increasing and is set to reach 67 by 2028. However, it’s crucial to check the exact State Pension age that applies to you, as it may differ based on your birth year.

National Insurance and State Pension Age

The general rule regarding National Insurance contributions after reaching the State Pension age is straightforward:

-

Employed Individuals: You no longer need to pay National Insurance contributions once you reach the State Pension age. This applies to Class 1 National Insurance contributions, which are deducted from your employment income.

-

Self-Employed Individuals: If you are self-employed, you are typically required to pay Class 2 and Class 4 National Insurance contributions. However, you stop paying Class 4 contributions at the end of the tax year in which you reach the State Pension age.

It’s important to note that this rule applies regardless of whether you choose to continue working after reaching the State Pension age or not.

Exceptions and Special Cases

While the general rule is clear, there are a few exceptions and special cases to be aware of:

-

Deferring State Pension: If you decide to defer claiming your State Pension, you will continue to pay National Insurance contributions until you start receiving your pension or reach the age of 70, whichever comes first.

-

Voluntary National Insurance Contributions: Even after reaching the State Pension age, you may choose to make voluntary National Insurance contributions to fill gaps in your National Insurance record. This can help increase your State Pension entitlement or qualify for certain benefits.

-

Employment with Multiple Jobs: If you have multiple jobs and reach the State Pension age while still working, you will no longer pay National Insurance on the earnings from your main job. However, you may still be required to pay National Insurance on the earnings from your secondary jobs.

Advantages of Paying National Insurance

While the prospect of no longer paying National Insurance contributions after reaching the State Pension age may sound appealing, it’s essential to consider the potential advantages of continuing to contribute:

-

Increased State Pension: By making voluntary National Insurance contributions, you can potentially increase your State Pension entitlement, which can translate into a higher retirement income.

-

Eligibility for Benefits: Certain benefits, such as Jobseeker’s Allowance or Employment and Support Allowance, may require you to have paid National Insurance contributions within a specific period before claiming them.

Conclusion

National Insurance Allowance Explained in Under 60 Seconds ⏱

FAQ

What are you entitled to when you turn 60 in the UK?

What is the pension age in the UK?

How much can a retired person earn without paying taxes UK?

What are the disadvantages of working after retirement in the UK?