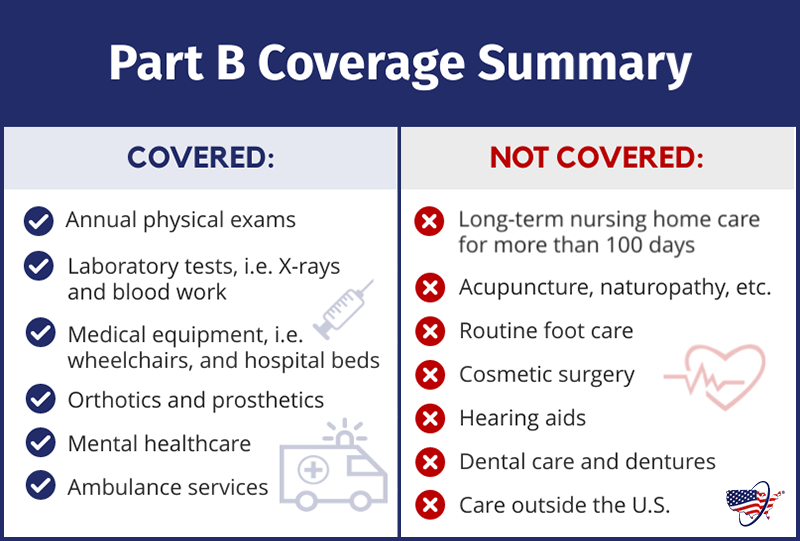

If you’re a Medicare beneficiary, understanding how Medicare Part B reimbursement works can be a daunting task. Medicare Part B covers a wide range of outpatient services, from doctor visits and preventive care to durable medical equipment and ambulance services. However, the reimbursement process can be confusing, with various terms and calculations determining how much you’ll pay out of pocket. In this article, we’ll break down the intricacies of Medicare Part B reimbursement, so you can make informed decisions about your healthcare.

Understanding the Deductible and Co-Insurance

Before Medicare Part B starts paying for covered services, you’ll need to meet an annual deductible. This deductible amount is set each year by the Centers for Medicare and Medicaid Services (CMS). For 2023, the Part B deductible is $226.

Once you’ve met the deductible, Medicare Part B will cover 80% of the “reasonable charge” for approved services. The “reasonable charge” is a predetermined reimbursement rate set by Medicare for various medical services and procedures.

The remaining 20% is your responsibility and is known as the “co-insurance.” This co-insurance amount is typically paid at the time of service or billed to you later.

Accepting Assignment: What It Means for Your Out-of-Pocket Costs

When a healthcare provider “accepts assignment,” it means they agree to accept Medicare’s approved reimbursement rate (the “reasonable charge”) as full payment for their services. In this scenario, you’re only responsible for the 20% co-insurance, and the provider cannot charge you more than the approved amount.

However, if a provider doesn’t accept assignment, they can charge you above the Medicare-approved rate. This additional amount is known as the “excess charge” or “balance billing.”

To protect beneficiaries from excessive charges, Medicare sets a “limiting charge” – the maximum amount a non-participating provider can bill for a covered service. The limiting charge is typically 115% of the Medicare-approved rate, though it can vary in some cases.

For example, let’s say your doctor charges $200 for a particular service, but Medicare’s approved rate is $150. If the doctor accepts assignment, you’ll pay just $30 (20% of $150). However, if they don’t accept assignment, they can charge up to $172.50 (115% of $150). In this case, your out-of-pocket cost would be $42.50 ($172.50 – $130, the amount Medicare pays).

The Part B Giveback Benefit

Some Medicare Advantage plans (Part C) offer a unique feature called the “Part B Giveback Benefit.” With this benefit, the plan carrier pays a portion or all of your monthly Part B premium, potentially saving you hundreds of dollars each year.

The Part B Giveback Benefit amount can range from a few cents to the full Part B premium cost, which is $164.90 per month in 2023 for most beneficiaries.

To be eligible for this benefit, you must:

- Be enrolled in both Part A and Part B of Original Medicare

- Pay your own Part B premium (it’s not deducted from your Social Security check)

- Live in the service area of a plan that offers the Part B Giveback Benefit

If you qualify, the reimbursement will either be credited to your Social Security check (if you pay your Part B premium that way) or reduce the amount you pay directly to Medicare.

Medigap Plans and Part B Reimbursement

Medicare Supplement Insurance plans (also known as Medigap plans) can help cover some of the out-of-pocket costs associated with Part B services. These private insurance plans work in conjunction with Original Medicare to cover deductibles, co-insurance, and excess charges (in some cases).

Different Medigap plans offer varying levels of coverage, so it’s essential to understand what each plan covers before enrolling. For example, Plan G covers the Part B deductible and co-insurance, while Plan F (no longer available to new enrollees) covers those costs and any excess charges from non-participating providers.

Staying Informed and Minimizing Costs

Medicare Part B reimbursement can be complex, but understanding the process can help you make informed decisions and minimize your out-of-pocket expenses. Here are some tips:

- Check if your healthcare providers accept Medicare assignment before receiving services.

- Consider enrolling in a Medicare Advantage plan with the Part B Giveback Benefit if available in your area.

- Explore Medigap plans to cover Part B deductibles, co-insurance, and excess charges.

- Review your Medicare Summary Notices (MSNs) carefully to ensure you’re not being overcharged.

- Don’t hesitate to appeal any questionable charges or denials.

By staying informed and proactive, you can navigate the complexities of Medicare Part B reimbursement and make the most of your healthcare coverage.

How to Get Medicare Part B Reimbursed.

FAQ

How do I get reimbursed for Medicare Part B?

How does Medicare Part B giveback work?

How does Medicare reimbursement work?

What is the $800 reimbursement for Medicare?