Life insurance is an essential tool for protecting your loved ones financially, but it’s crucial to understand the duration of your commitment. The length of time you’re tied into a life insurance policy can vary significantly depending on the type of coverage you choose. In this article, we’ll explore the different types of life insurance and how long you’re obligated to keep them.

Term Life Insurance: Temporary Protection

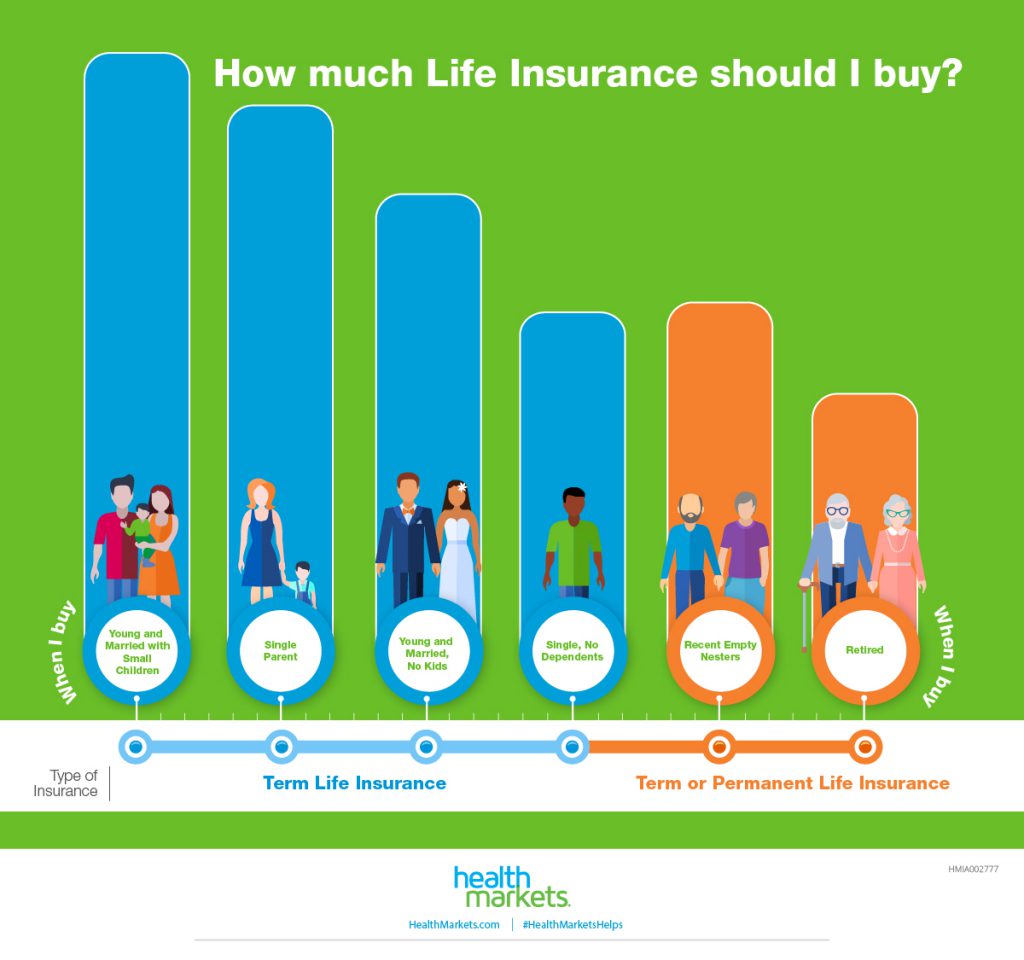

Term life insurance provides coverage for a specific period, typically ranging from 1 to 30 years. When you purchase a term life policy, you’re essentially committing to the coverage for the duration of the term you select. Here’s how it works:

- You choose the term length (e.g., 10 years, 20 years, 30 years)

- You pay premiums for the duration of the term

- If you pass away during the term, your beneficiaries receive the death benefit

- If you survive the term, the policy expires, and you have the option to renew or purchase a new policy

The beauty of term life insurance is its temporary nature. You’re not locked into a lifelong commitment, making it an affordable option for those seeking coverage during specific life stages, such as raising a family or paying off a mortgage.

Whole Life Insurance: A Lifelong Commitment

Whole life insurance, on the other hand, is a permanent form of coverage designed to last your entire lifetime. When you purchase a whole life policy, you’re essentially committing to pay premiums until you pass away or cash out the policy.

Here are the key points about whole life insurance:

- Premiums remain level throughout your life

- The policy accumulates cash value over time, which you can borrow against or withdraw

- Some whole life policies pay dividends, which you can receive in cash, reinvest, or use to pay premiums

- Coverage remains in effect for your entire life, as long as you continue paying premiums

It’s important to note that whole life insurance premiums are typically higher than term life premiums, as you’re paying for lifelong coverage and the cash value component.

Universal Life Insurance: Flexible Lifelong Coverage

Universal life insurance is another type of permanent life insurance that offers more flexibility than whole life. With universal life, you have the ability to adjust your premiums and death benefit amounts as your needs change over time.

Key features of universal life insurance:

- Premiums are flexible, allowing you to increase or decrease payments

- The death benefit can be adjusted as needed

- The policy accumulates cash value, which earns interest based on current market rates

- Coverage remains in effect until a specified maturity age (e.g., 95 or 100), as long as the cash value is sufficient to cover the costs

While universal life insurance provides more flexibility, it’s still a lifelong commitment. You’ll need to continue making premium payments or maintain sufficient cash value to keep the policy in force.

Policy Lapses and Reinstatement

Regardless of the type of life insurance you have, it’s crucial to understand the consequences of missing premium payments. If you fail to pay your premiums within the grace period (typically 30-31 days), your policy may lapse, and your coverage will terminate.

However, most insurers offer the option to reinstate a lapsed policy within a certain timeframe, usually up to five years. To reinstate your policy, you’ll need to pay any outstanding premiums, along with interest, and potentially undergo a new medical examination.

Making Changes or Replacing a Policy

If your life circumstances change, you may consider modifying or replacing your existing life insurance policy. However, it’s essential to approach this cautiously, as replacing a policy can have significant implications:

- New policies typically have a new contestability period (usually two years), during which the insurer can investigate and potentially deny a death benefit claim.

- Permanent life insurance policies may have surrender charges or tax consequences if you cash them out prematurely.

- You may need to undergo a new medical examination, which could result in higher premiums or denial of coverage if your health has deteriorated.

Before making any changes to your life insurance policy, it’s advisable to consult with a licensed insurance agent or financial advisor to understand the potential consequences and ensure you’re making an informed decision.

Selling Your Life Insurance Policy

In some cases, you may have the option to sell your life insurance policy to a third party, known as a life settlement provider. This option is typically available if you have a terminal illness or have outlived your retirement savings and need cash.

Life settlement providers will pay you a percentage of the policy’s death benefit, ranging from 10% to 75%, depending on factors such as your life expectancy and the policy’s premiums.

It’s important to note that selling your life insurance policy may have tax implications, and the income from a life settlement could affect your eligibility for government programs like Medicaid. It’s advisable to consult with an attorney or financial advisor before pursuing a life settlement.

Conclusion

The length of time you’re tied into a life insurance policy depends on the type of coverage you choose. Term life insurance provides temporary protection for a specific period, while whole life and universal life insurance are lifelong commitments, as long as you continue paying premiums.

Understanding the duration of your life insurance policy is crucial for making informed decisions about your coverage and ensuring you have the right protection in place for your loved ones. If you’re unsure about the specifics of your policy or considering making changes, consult with a licensed insurance professional or financial advisor for guidance.

How long should term life insurance last?

FAQ

How long do you have to have life insurance before you can pull from it?

How many years do you have to pay into a life insurance policy?

At what age does your life insurance end?

What happens after 20 years of paying life insurance?