When it comes to the Affordable Care Act, also known as Obamacare, understanding how your income is calculated can be a crucial factor in determining your eligibility for health insurance subsidies and cost-saving programs. Many individuals wonder if the calculation is based on their adjusted gross income (AGI), a familiar term from their tax returns. In this comprehensive guide, we’ll demystify the concept of modified adjusted gross income (MAGI) and explore how it relates to the Affordable Care Act.

What is Modified Adjusted Gross Income (MAGI)?

The Affordable Care Act uses a specific income calculation called the modified adjusted gross income (MAGI) to determine eligibility for premium tax credits and other cost-sharing reductions. MAGI is not a line item on your tax return; rather, it’s a calculation derived from your total (or “gross”) income for the tax year, with certain adjustments allowed.

According to the Centers for Medicare & Medicaid Services (CMS), MAGI is defined as follows:

Modified Adjusted Gross Income (MAGI) = Adjusted Gross Income (AGI) + Untaxed Foreign Income + Non-Taxable Social Security Benefits (including Tier 1 Railroad Retirement Benefits) + Tax-Exempt Interest

In simpler terms, MAGI starts with your Adjusted Gross Income (AGI), which is the amount you report on Line 11 of your Form 1040 tax return. It then adds back certain types of income that are typically excluded from AGI, such as untaxed foreign income, non-taxable Social Security benefits, and tax-exempt interest.

It’s important to note that MAGI differs from AGI in that it includes certain income sources that may not be taxable, but are still considered countable income for the purposes of the Affordable Care Act.

Why Does Obamacare Use MAGI Instead of AGI?

The decision to use MAGI instead of AGI for determining Affordable Care Act subsidies and program eligibility was made to ensure a more comprehensive and accurate assessment of an individual’s or household’s financial situation. By including non-taxable income sources, MAGI provides a more complete picture of a person’s ability to afford health insurance premiums and out-of-pocket costs.

Additionally, using MAGI helps streamline the application process and align with the eligibility criteria used for other government assistance programs, such as Medicaid and the Children’s Health Insurance Program (CHIP).

Calculating MAGI for Obamacare

To calculate your MAGI for the purposes of the Affordable Care Act, you’ll need to follow these steps:

-

Start with your Adjusted Gross Income (AGI): This is the amount reported on Line 11 of your Form 1040 tax return.

-

Add back non-taxable Social Security benefits: If you received Social Security benefits during the tax year, add the non-taxable portion of those benefits to your AGI. This includes Tier 1 Railroad Retirement benefits.

-

Add back tax-exempt interest: If you earned any interest from tax-exempt sources, such as municipal bonds or certain investments, add that amount to your AGI.

-

Add back untaxed foreign income: If you earned income from foreign sources that was not subject to U.S. taxes, add that amount to your AGI.

The result of this calculation is your MAGI, which will be used to determine your eligibility for premium tax credits, cost-sharing reductions, and other Affordable Care Act benefits.

Reporting Changes in MAGI

It’s important to note that your MAGI is based on your projected income for the year in which you’re seeking coverage. If your income changes during the year, you must report those changes to the Health Insurance Marketplace or your state’s Medicaid agency. Failing to report changes in your MAGI could result in receiving the wrong amount of financial assistance, which may need to be reconciled when filing your tax return.

Conclusion

While the Affordable Care Act does not directly use your Adjusted Gross Income (AGI) from your tax return, it relies on a similar calculation called the modified adjusted gross income (MAGI). By including non-taxable income sources, MAGI provides a more comprehensive assessment of an individual’s or household’s financial situation, ensuring that subsidies and cost-sharing reductions are accurately allocated.

Understanding how MAGI is calculated and reported is crucial for navigating the Affordable Care Act’s financial assistance programs. By staying informed and reporting any changes in your income promptly, you can ensure that you receive the appropriate level of support and avoid potential complications down the line.

Is Obamacare based on adjusted gross income?

FAQ

Does Obamacare look at adjusted gross income?

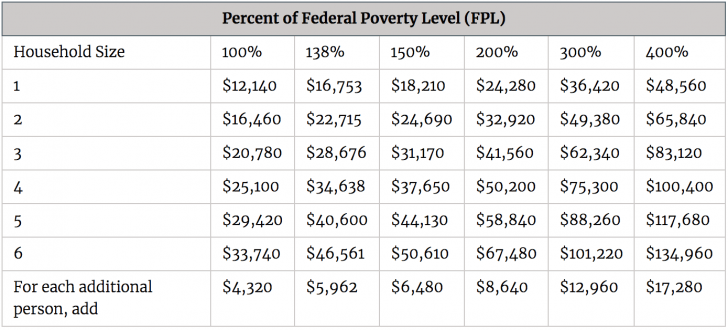

What is the highest income to qualify for Obamacare?

|

Household size

|

Min. income

|

Typical max. income

|

|

1 person

|

$14,580

|

$58,320

|

|

2

|

$19,720

|

$78,880

|

|

3

|

$24,860

|

$99,440

|

|

4

|

$30,000

|

$120,000

|

How do I estimate my income for Obamacare?

What income is used to determine Affordable Care Act?