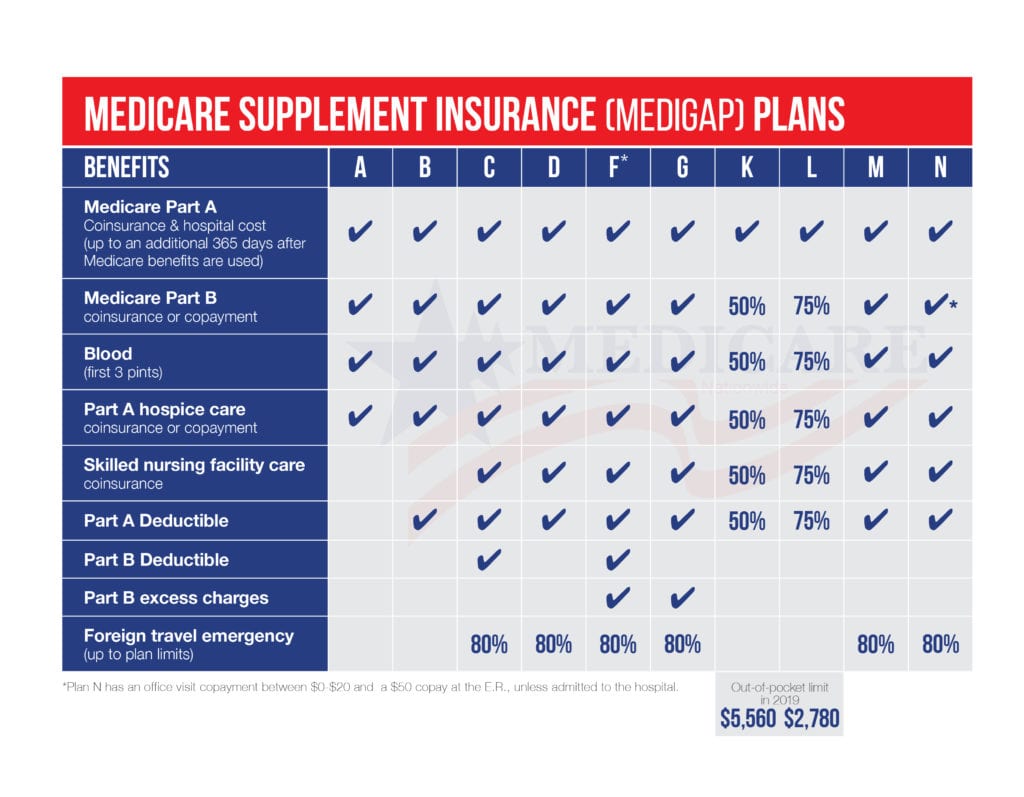

Navigating the world of Medicare can be confusing, especially when it comes to Medicare Supplement Plans, also known as Medigap plans. These plans are designed to help cover some of the out-of-pocket costs that Original Medicare doesn’t cover, such as deductibles, copayments, and coinsurance. However, there are specific rules and requirements you need to meet to be eligible for a Medigap plan. In this article, we’ll break down the rules and provide you with a comprehensive guide to understanding the eligibility criteria for Medicare Supplement Plans.

Eligibility Requirements

To be eligible for a Medigap plan, you must meet the following criteria:

-

Enrollment in Medicare Parts A and B: You must be enrolled in both Medicare Part A (hospital insurance) and Part B (medical insurance) to qualify for a Medigap plan. These plans are designed to work alongside Original Medicare, so having both parts is essential.

-

Age Requirement: In most states, you must be 65 years old or older to purchase a Medigap plan. However, some states allow individuals under 65 who are eligible for Medicare due to a disability or certain medical conditions to enroll in a Medigap plan.

-

Residency Requirement: You must reside in the state where the Medigap plan is offered at the time of application. Medigap plans are regulated at the state level, so the availability and cost of plans can vary from one state to another.

-

Medical Underwriting: In most cases, you will need to undergo medical underwriting, which involves answering health-related questions and providing access to your medical records. This process helps insurance companies determine your eligibility and the appropriate premium rate based on your health status. However, there are certain periods known as “Guaranteed Issue Rights” when medical underwriting is not required, which we’ll discuss later.

Guaranteed Issue Rights

Guaranteed Issue Rights are periods or situations where insurance companies are required to sell you a Medigap plan without medical underwriting and cannot charge you a higher premium based on pre-existing conditions. These rights typically apply in the following situations:

-

Medigap Open Enrollment Period: This is the six-month period that starts on the first day of the month you turn 65 and are enrolled in Medicare Part B. During this period, you have the right to purchase any Medigap plan available in your state without being subject to medical underwriting or facing higher premiums due to pre-existing conditions.

-

Losing Employer or Group Health Coverage: If you lose your employer or group health coverage, you may have a Guaranteed Issue Right to purchase a Medigap plan without medical underwriting.

-

Moving Out of a Plan’s Service Area: If you move out of the service area of your Medicare Advantage Plan or Medicare SELECT plan, you have the right to purchase a Medigap plan without medical underwriting.

-

Other Specific Situations: There are additional situations that may qualify you for Guaranteed Issue Rights, such as your Medicare Advantage Plan leaving Medicare, your plan misled you or violated its rules, or your health care provider has left your plan’s network.

It’s important to note that these Guaranteed Issue Rights have specific time frames and requirements, so it’s crucial to understand them and act promptly if you find yourself in one of these situations.

Best Time to Enroll in a Medigap Plan

The best time to enroll in a Medigap plan is during your Medigap Open Enrollment Period, which begins on the first day of the month you turn 65 and are enrolled in Medicare Part B. This six-month window is crucial because it’s the only time you have a guaranteed right to purchase any Medigap plan available in your state without medical underwriting or facing higher premiums due to pre-existing conditions.

If you miss this initial Medigap Open Enrollment Period, you may still be able to purchase a Medigap plan, but insurance companies can deny coverage or charge higher premiums based on your health status and pre-existing conditions.

Pre-Existing Condition Waiting Periods

Even if you enroll in a Medigap plan during your Medigap Open Enrollment Period, some plans may still impose a pre-existing condition waiting period. This means that the plan will not cover costs related to any pre-existing conditions you have for a certain period, typically six months.

However, if you had creditable coverage (such as employer-sponsored health insurance or a Medicare Advantage Plan) before enrolling in Medicare, the pre-existing condition waiting period may be reduced or eliminated entirely.

Switching or Dropping Your Medigap Plan

Once you have a Medigap plan, you can switch to a different plan or drop your current plan at any time. However, if you decide to switch or drop your plan outside of your Medigap Open Enrollment Period or a Guaranteed Issue Right period, you may be subject to medical underwriting and potentially denied coverage or charged higher premiums based on your health status.

It’s important to carefully consider your options and timelines when making changes to your Medigap plan to avoid potential gaps in coverage or unexpected costs.

State-Specific Variations

It’s important to note that while Medigap plans are standardized at the federal level, some states may have additional rules and regulations regarding Medigap plan eligibility and enrollment. It’s always a good idea to check with your State Health Insurance Assistance Program (SHIP) or your state’s insurance department to understand any state-specific requirements or variations that may apply to you.

Conclusion

Understanding the rules and eligibility criteria for Medicare Supplement Plans is crucial to ensuring you have the right coverage and avoiding potential gaps or unexpected costs. By following the guidelines outlined in this article, you can navigate the process of enrolling in a Medigap plan with confidence and make informed decisions about your healthcare coverage needs.

Remember, the best time to enroll is during your Medigap Open Enrollment Period, which offers guaranteed issue rights and protects you from medical underwriting or higher premiums due to pre-existing conditions. If you miss this window, you may still be able to enroll, but the process may be more challenging and costly.

Don’t hesitate to seek assistance from trusted resources, such as your State Health Insurance Assistance Program (SHIP) or a licensed insurance agent, if you have any questions or need additional guidance throughout the process.

Medicare Explained – Medicare Supplement Plans ✅

FAQ

Can you be denied a Medicare Supplement plan?

What are the criterias of a Medicare Supplement plan?

Can you enroll in Medicare Supplement plans at any time?

What disqualifies you from Medigap?