In the realm of health insurance, the term “PPO” often pops up, leaving many individuals scratching their heads. What exactly is a PPO, and how does it differ from other healthcare plans? In this comprehensive guide, we’ll delve into the intricacies of Preferred Provider Organizations (PPOs) and explore why they might be a suitable option for your healthcare needs.

Defining PPO: The Preferred Provider Organization Explained

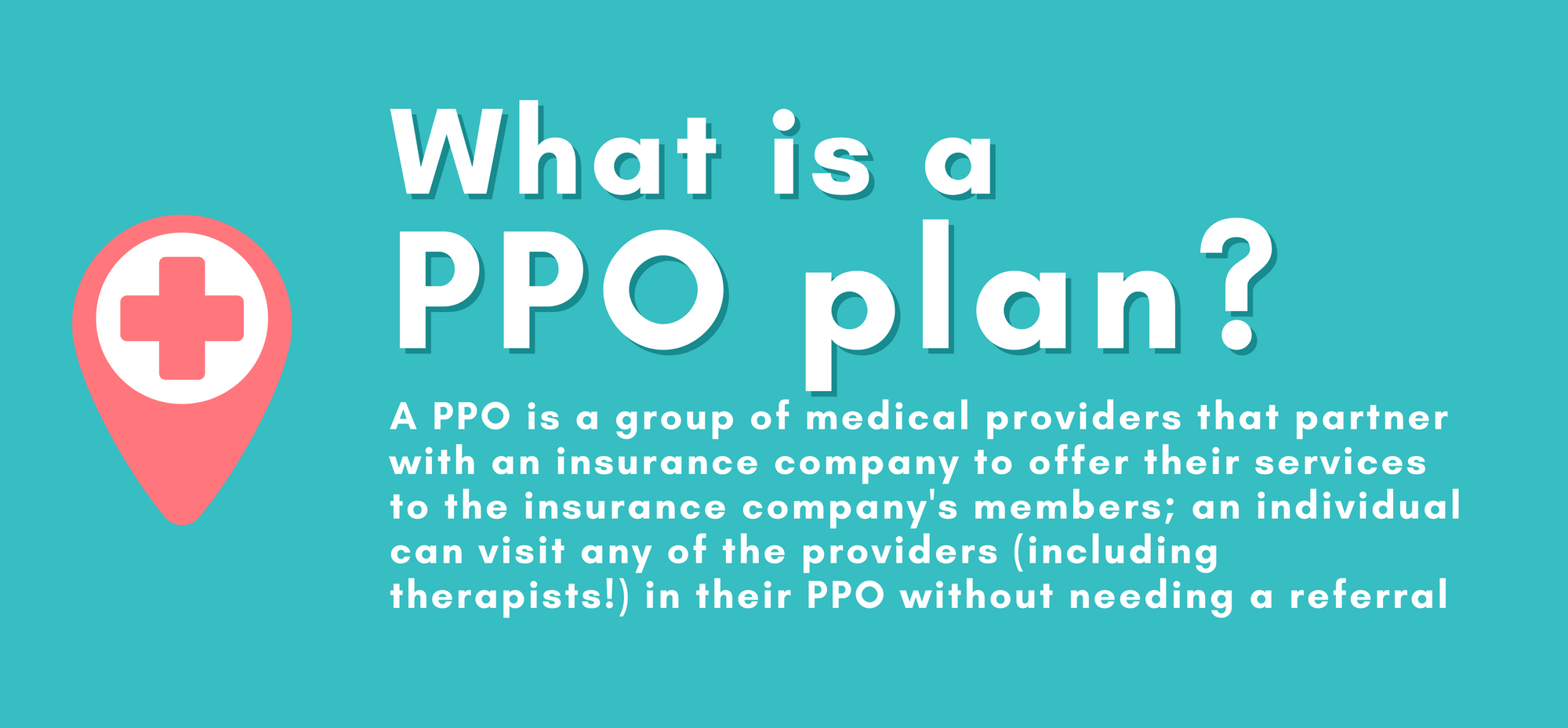

The acronym PPO stands for “Preferred Provider Organization.” It is a type of health insurance plan that provides coverage to participants through a network of pre-selected healthcare providers, such as hospitals, physicians, and specialists. These providers have agreed to offer their services at discounted rates, which are negotiated by the insurance company.

In a PPO plan, participants have the flexibility to seek medical care from both in-network and out-of-network providers. However, using in-network providers typically results in lower out-of-pocket costs, such as copays and deductibles, making it a more cost-effective option.

Key Features of PPO Plans

To better understand how PPOs work, let’s explore some of their key features:

-

Provider Network: PPOs establish a network of preferred healthcare providers, including hospitals, doctors, specialists, and other medical facilities. These providers have agreed to offer their services at pre-negotiated, discounted rates to PPO members.

-

In-Network vs. Out-of-Network: PPO plans allow participants to receive care from both in-network and out-of-network providers. In-network providers typically charge lower copays and coinsurance rates, while out-of-network providers may result in higher out-of-pocket expenses.

-

Referrals Not Required: Unlike Health Maintenance Organizations (HMOs), PPOs generally do not require referrals from a primary care physician (PCP) to see specialists. This added flexibility allows PPO members to seek care from specialists directly, without going through the referral process.

-

Deductibles and Coinsurance: PPO plans often have deductibles that must be met before the insurance company begins to cover a portion of the costs. Additionally, members may be responsible for coinsurance, which is a percentage of the total cost of medical services they must pay, even after meeting the deductible.

-

Premiums: PPO plans typically have higher monthly premiums compared to HMOs, reflecting the increased flexibility and broader provider networks they offer.

Advantages of PPO Plans

PPOs offer several advantages that may make them an attractive choice for individuals seeking comprehensive healthcare coverage:

-

Flexibility: The ability to seek care from both in-network and out-of-network providers provides greater flexibility, especially when traveling or in need of specialized care.

-

No Referrals Required: PPO members can directly access specialists without the need for referrals from a primary care physician, streamlining the process of receiving specialized care.

-

Extensive Provider Networks: PPOs typically have larger networks of healthcare providers compared to HMOs, offering a wider range of options for members.

-

Nationwide Coverage: Many PPO plans provide nationwide coverage, allowing members to receive care from in-network providers across the country, making them a suitable choice for frequent travelers or those with multiple residences.

Potential Drawbacks of PPO Plans

While PPOs offer numerous benefits, it’s essential to consider their potential drawbacks as well:

-

Higher Costs: PPO plans generally have higher monthly premiums, deductibles, and out-of-pocket expenses compared to HMOs, especially when using out-of-network providers.

-

Lack of Coordination: Unlike HMOs, PPOs do not typically require a primary care physician to coordinate care, which may result in less oversight and continuity of care.

-

Confusion over Provider Networks: Navigating provider networks and determining whether a healthcare provider is in-network or out-of-network can be challenging, potentially leading to higher out-of-pocket costs if not carefully managed.

Making an Informed Decision

When choosing a healthcare plan, it’s crucial to carefully evaluate your specific needs, budget, and preferences. PPOs may be a suitable choice for individuals who value flexibility, access to a wider range of providers, and the ability to seek care without referrals. However, it’s essential to consider the potential higher costs associated with PPO plans, especially when using out-of-network providers.

Before enrolling in a PPO plan, thoroughly review the plan details, including the provider network, copays, deductibles, and coinsurance rates. Additionally, consult with healthcare professionals, insurance advisors, or employer-sponsored benefits counselors to ensure you make an informed decision that aligns with your healthcare needs and financial considerations.

By understanding the intricacies of PPOs and weighing their advantages and disadvantages, you can make an informed choice and secure comprehensive healthcare coverage that best suits your unique circumstances.

What is a PPO?

FAQ

Which is better a PPO or HMO?

What does PPO mean in healthcare?

What does PPO mean in a job?

Why should I choose a PPO?