As we navigate the complexities of healthcare in our golden years, understanding the costs associated with Medicare Part D, the prescription drug coverage plan, becomes increasingly important. With countless Americans relying on this crucial program, the question on everyone’s mind is: “What is the average cost for Medicare Part D?”

The Basics of Medicare Part D

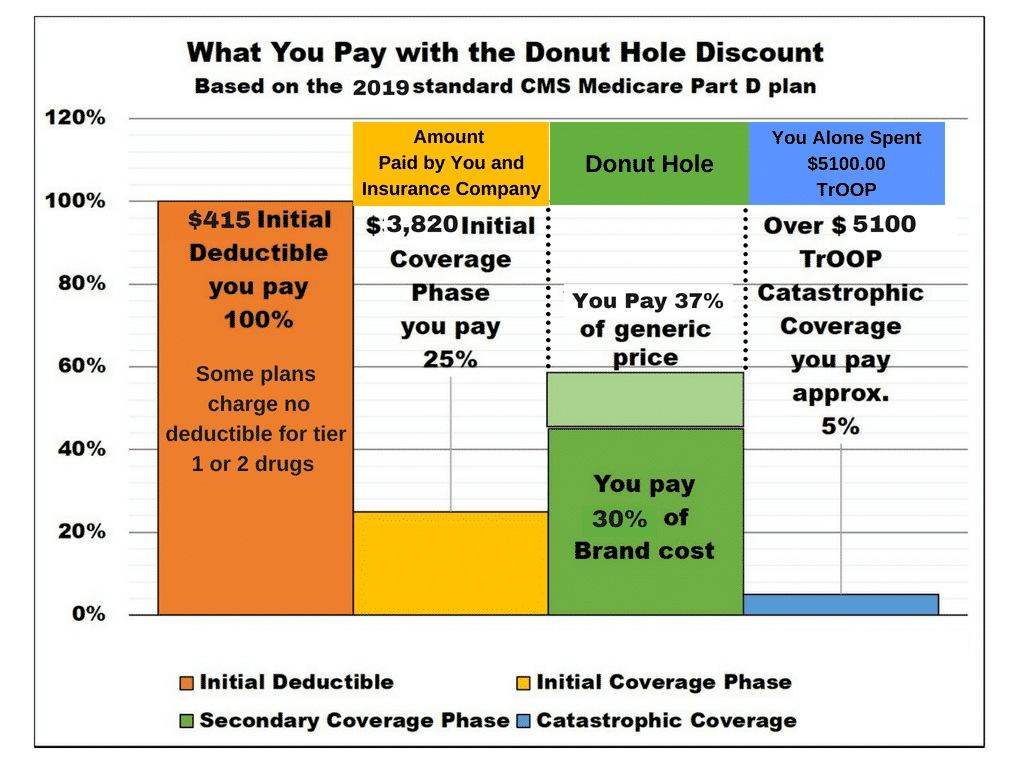

Before delving into the nitty-gritty of costs, let’s quickly review Medicare Part D. This optional program provides coverage for prescription drugs, helping beneficiaries manage the often-steep expenses associated with necessary medications. While Part A (hospital insurance) and Part B (medical insurance) cover other aspects of healthcare, Part D focuses specifically on prescription drugs.

The Average Cost: A Breakdown

According to the latest data for 2024, the average monthly premium for a basic Medicare Part D plan stands at $59. However, it’s important to note that costs can vary significantly, ranging from $0 to a whopping $195 per month. This wide range highlights the importance of carefully evaluating and selecting the plan that best suits your individual needs and budget.

Additional Costs to Consider

While the monthly premium is the most visible cost associated with Medicare Part D, it’s not the only expense you might encounter. Here are some additional fees to keep in mind:

-

Late Enrollment Penalty: If you didn’t enroll in Medicare Part D when you were first eligible and went without creditable prescription drug coverage for 63 consecutive days or more, you may face a late enrollment penalty. This penalty is calculated based on the number of months you went without coverage and is added to your monthly premium.

-

Income-Related Adjustments: Medicare beneficiaries with higher incomes may be required to pay an additional amount, known as the Income-Related Monthly Adjustment Amount (IRMAA). This adjustment is based on your modified adjusted gross income reported on your IRS tax return from two years prior.

To give you an idea of the potential impact, here’s a table illustrating the IRMAA for Medicare Part D in 2024:

| Filing Status | Yearly Income in 2022 | Monthly IRMAA in 2024 |

|---|---|---|

| Individual | $103,000 or less | $0 |

| Individual | Above $103,000 up to $129,000 | $12.90 + plan premium |

| Individual | Above $129,000 up to $161,000 | $33.30 + plan premium |

| Individual | Above $161,000 up to $193,000 | $53.80 + plan premium |

| Individual | Above $193,000 and less than $500,000 | $74.20 + plan premium |

| Individual | $500,000 or above | $81.00 + plan premium |

| Joint | $206,000 or less | $0 |

| Joint | Above $206,000 up to $258,000 | $12.90 + plan premium |

| Joint | Above $258,000 up to $322,000 | $33.30 + plan premium |

| Joint | Above $322,000 up to $386,000 | $53.80 + plan premium |

| Joint | Above $386,000 and less than $750,000 | $74.20 + plan premium |

| Joint | $750,000 or above | $81.00 + plan premium |

It’s important to note that these adjustments can change annually, so it’s always wise to stay informed about any updates.

Factors Influencing Part D Costs

While the average cost provides a general guideline, several factors can influence the actual amount you’ll pay for your Medicare Part D coverage. These include:

- Plan Type: Basic plans typically have lower premiums, while enhanced plans offering additional coverage may come with higher premiums.

- Prescription Drug Needs: The more medications you require, the higher your overall costs may be, depending on your plan’s formulary and cost-sharing structure.

- Location: Costs can vary based on your geographic location, as plans may tailor their offerings and pricing to specific regions.

- Plan Provider: Different insurance companies offering Medicare Part D plans may have varying premium rates and cost structures.

Strategies to Manage Part D Costs

While Medicare Part D can be a financial burden for some, there are strategies you can employ to manage these costs more effectively:

- Shop Around: During the annual enrollment period, take the time to compare various plans and their coverage details. Even a slight difference in premiums or cost-sharing can add up over time.

- Consider Generic Alternatives: When possible, opt for generic versions of prescription drugs, which can significantly reduce your out-of-pocket expenses.

- Utilize Prescription Assistance Programs: Many pharmaceutical companies offer assistance programs for individuals who meet certain income criteria, helping to offset the costs of their medications.

- Explore Part D Plans with Lower Premiums: If you have a limited medication regimen, consider plans with lower premiums but higher cost-sharing, as they may be more cost-effective in the long run.

By understanding the average cost of Medicare Part D and the various factors that influence it, you can make informed decisions and better manage your healthcare expenses during retirement. Remember, staying vigilant and proactive can go a long way in ensuring you have access to the prescription drugs you need without breaking the bank.

How much does it cost for Medicare Part D

FAQ

What is the average monthly cost of Medicare Part D?

Is Medicare Part D worth it?

How much will Medicare Part D cost in 2024?

Does everyone pay for Medicare Part D?